Present value of minimum lease payments

Lease liability represents the current value of minimum future lease payments. The discount rate can be the rate implicit in the lease which is the rate where lease payments and unguaranteed residual value are equal to the fair value of the asset and its associated costs for.

Minimum Lease Payment Overview How To Calculate Example

To calculate it you need to make assumptions about.

. For example you could use this formula to calculate the present value of your future rent payments as specified in your lease. Payments probable of being owed by the lessee as the result of a residual value guarantee. Lets say you pay 1000 a month in rent.

2 Calculation of present value PV of min finance lease payments. At commencement of the lease term finance leases should be recorded as an asset and a liability at the lower of the fair value of the asset and the present value of the minimum lease payments discounted at the interest rate implicit in the lease if practicable or else at the entitys incremental borrowing rate IAS 1720. The present value of the minimum lease payments totals at least 90 of the fair value of the asset at the beginning of the lease.

This is your right-of-use assent and the lease liability at the commencement date. The lessor uses the residual value to determine the periodic lease payments the lessee must make on the asset. Accounting for Variable Lease Payments.

Annual lease rents P 500000. Below is an example of using an annuity to solve the above problem. The outcome of the lease analysis is rarely accidental.

Depending on the agreement the lessee may be able to make. It holds because the periodicity of the lease payments is typically evenly spaced out. Fixed consideration is a payment made directly for the right to use the underlying asset and is explicitly stated in the lease contract.

For example the present value of the minimum lease payments may approximate to the fair value of the asset at the inception of the final lease and there is unlikely to be an option to purchase the asset at fair value or to extend the lease at a market rent because the asset has reached the end of its life. The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. For example if the present value of the lease payments amounts to 50000 then 50000 is going to be debited to the relevant asset account whereas the.

Lease payments can be separated into two categories. The ClearTax Lease Calculator uses the residual value of the asset to calculate both the monthly lease payments and the total. GAAP leases are finance leases if any of four conditions are met.

Fixed and variable consideration. The present value of the minimum lease payments - at the beginning of the lease term - is equal to or greater than 90 of the original fair market value of the equipment. The maturity analysis for operating leases should not be combined with the maturity analysis for sales-type and direct financing leases.

The present value of the minimum lease payments required under the lease is at least 90 of the fair value of the asset at the inception of the lease. The net investment value is calculated by discounting the minimum lease payments at the implicit interest rate. Lets suppose if you have agreed to pay 1 of.

The formula of PV PV P 1 1i-n i Given. For leases classified as capital lessees perform a calculation to determine the present value of minimum lease payments that is used as a basis for the capital lease asset and liability values. I am assuming that he meant the landlord securing minimum lease payment.

The lessor and lessee typically agree upon lease conditions in advance that will designate a lease as an operating lease or capital lease. The present value of the minimum lease payments required under the lease is at least 90 of the fair value of the asset that exists at the beginning of the lease contract. As a rule of thumb a lease may require 30 or 60 days notice according to the states landlord-tenant laws.

An equipment lease agreement is between a lessor the owner of the equipment and a lessee who agrees to pay rent for the equipment to use for a specified time period. 100 1 1 5 -3 5 27232. The system automatically calculates the monthly interest expense on.

The fourth condition requires capitalization if the present value of minimum lease payments MLP is greater than 90 of. Review the lease to ensure that a tenant is providing enough notice that a lease is not being renewed. CR Lease Liability 136495.

PV of Annuity of Annual Lease Payments. Now that weve explained the different ways accounting principles look at equipment leasing lets answer a few common questions. If a lease agreement contains any one of the preceding four criteria the lessee records it as a capital lease.

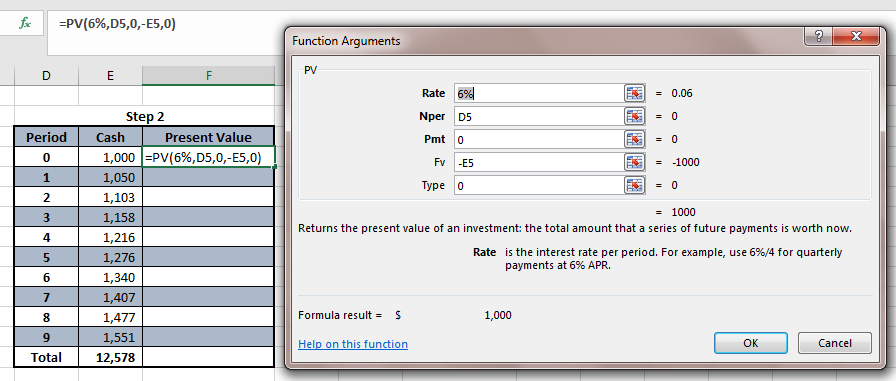

Is the present value of lease payments plus RVG residual value guaranteed by the lessee. Within ASC 840-10-25-6 this standard defines minimum lease payments as the financial obligations that a lessee must make in connection with the leased. Our monthly rate is 025 and the present value of all monthly lease payments over 5 years is CU 55 708.

However the asset will obviously be. Accounting for a Capital Lease and Operating Lease. A maturity analysis of lease payments showing the undiscounted cash flows to be received on an annual basis for a minimum of the next five years and the total lease payments to be received in the remaining years.

Calculating present value of future payments Using these assumptions you need to calculate the present value of the minimum future lease payments. Distribute the cash received as periodic lease rentals into two parts. Present value test.

Updated July 28 2022. An equipment lease can be structured with a start and end date or on a month-to-month basis. Verify that the tenant is giving sufficient notice not to renew a lease.

Ask the tenant to send a lease non-renewal letter. The likely amounts owed under residual value guarantee. Present value of future minimum lease payments As was previously mentioned the straight-line lease expense is calculated as the sum of all payments divided by the lease term.

Calculating the present value of minimum lease payments can also be achieved using an annuity formula. You would recognize it as.

Asc 842 Lease Amortization Schedule Templates In Excel Free Download

Calculate Lease Payments Tvmcalcs Com

Chartered Tax Advisers And Chartered Accountants

C H A P T E R 21 Accounting For Leases Ppt Video Online Download

Calculating Present Value In Excel Function Examples

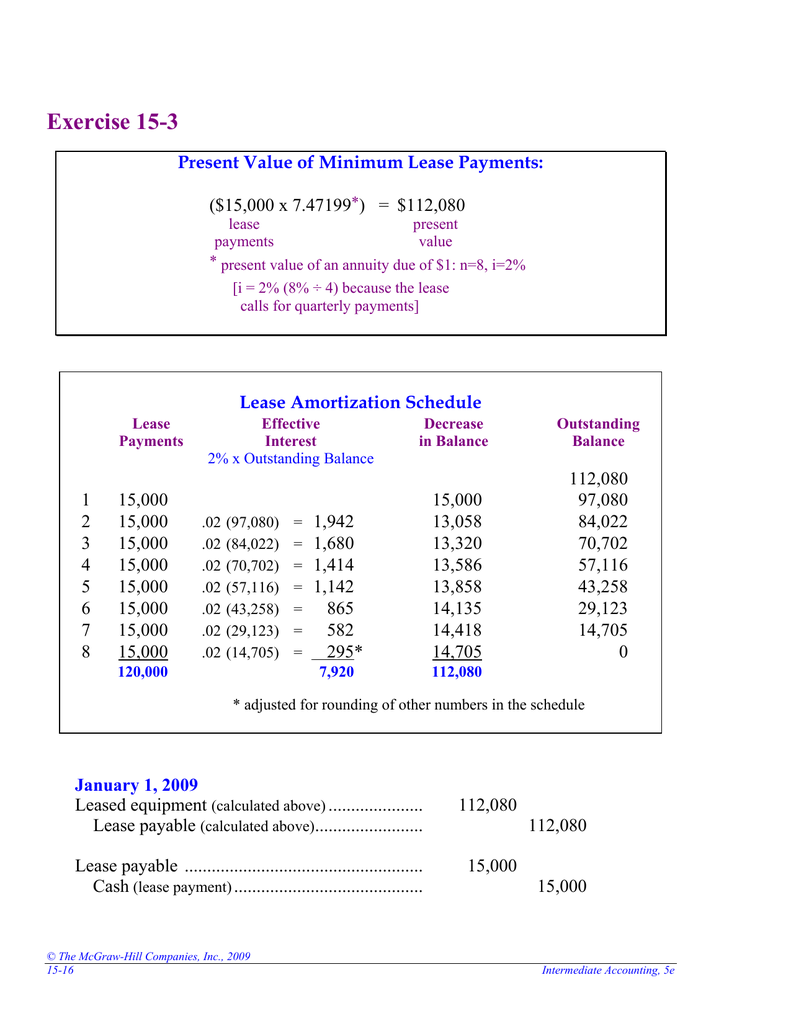

Exercise 15 3 Present Value Of Minimum Lease Payments 15 000 X 7 47199

21 Chapter Accounting For Leases Intermediate Accounting 12th Edition Ppt Video Online Download

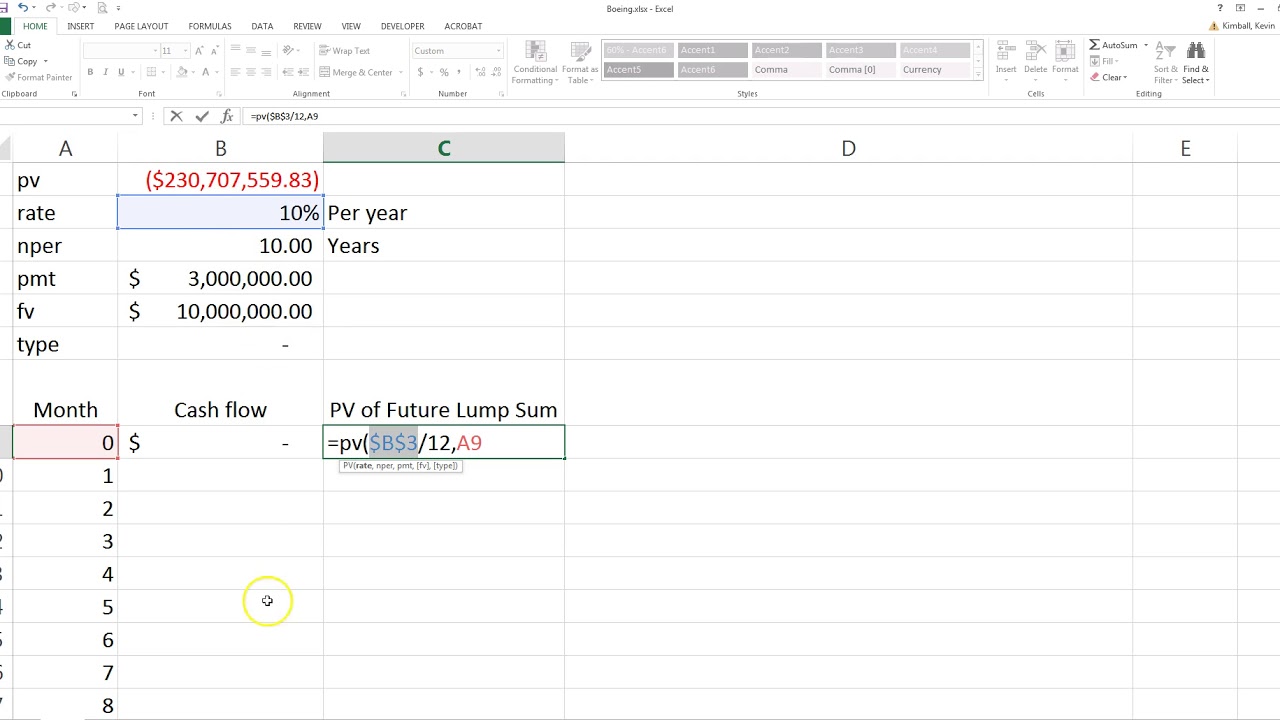

How To Calculate The Present Value Of Lease Payments In Excel

Accounting For Leases Acctg 5120 David Plumlee Ppt Download

Lease Classification Cornell University Division Of Financial Affairs

Lease Payment Example And Lease Payment In Income Statement

How To Calculate The Present Value Of Lease Payments In Excel

Aca Learning Center 10 Steps To Unlocking An Understanding Of Lease Accounting Part 1

21 1 Volume C H A P T E R 21 Accounting For Leases Intermediate Accounting Ifrs Edition Kieso Weygandt And Warfield Ppt Download

Compute The Present Value Of Minimum Future Lease Payments Youtube

Using Excel To Calculate Present Value Of Minimum Lease Payments Thebrokerlist Blog

Intermediate Accounting Kieso Weygandt Warfield Ppt Download